OFF BALANCE

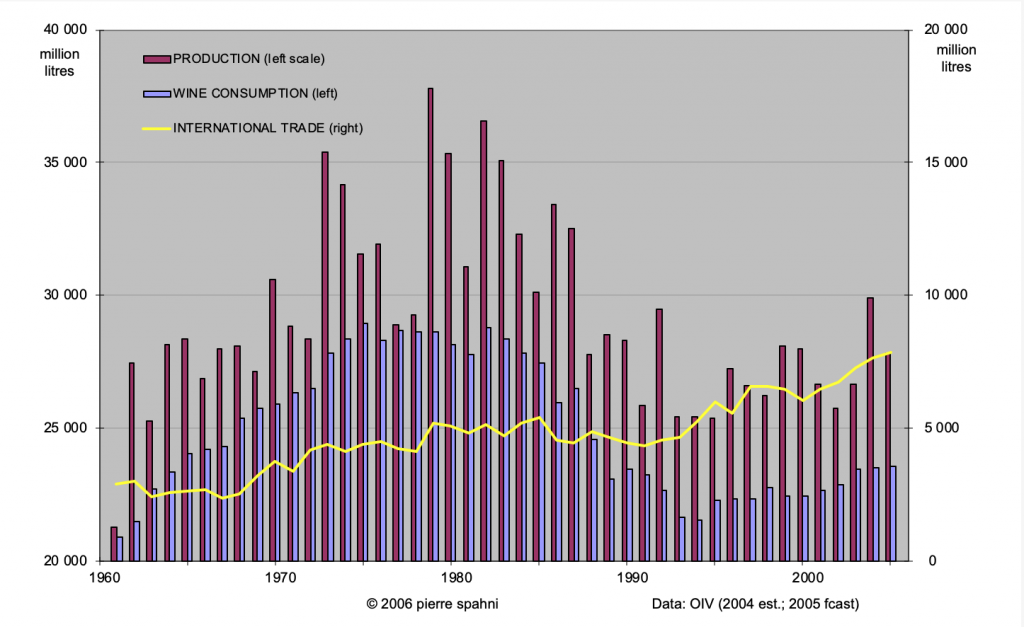

The reversal of a 15-year-old downward trend in world demand for wine, in the mid-1990s, was the combined result of a resumption of growth in the US, fast expanding consumption in the UK (wine is displacing beer in both countries), and the emergence of new markets along Asia’s Pacific Rim, particularly in China, which introduced a policy of favouring wine over spirits consumption a decade ago (to combat alcoholism). These gains were large enough to offset the continuing decline in demand in Southern Europe and Argentina. The average rate of growth over the past ten years was less than one percent per annum [1].

Producers’ reaction was swift: some decided to plant on a grand scale (Australia) whilst the EU shelved its efforts to balance supply with demand. With old-style consumers on the wane and many new customers trading up from their unsophisticated entry-level wines, basic products have become a much harder sell without the help of state subsidies or heavy promotional discounts. Supply grew at a yearly rate of over one percent on average, slightly faster than demand, leaving surpluses to develop on a regional basis – just as predicted [2].

Surplus-laden Spain and Australia got out best from the mêlée, thanks to more aggressive pricing, and now boast shares of nearly ten and twenty percent of world trade respectively. This puts Spain at par with Italy and France, who exported nearly three times as much as it did when joining the EU but felt no particular need for developing international brands (and cross-border consolidation) in order to fight off the ever-growing bargaining power of food retailers operating across national markets. Trade volumes were boosted by the generally tougher international competition and grew at over three percent a year, to reach about 7’800 million litres in 2005 [3].

The yawning gap between production and consumption (4’500 million litres over the past ten years as well as in 2005) is partly filled by wines used for EU-subsidised distillation into brandies and the manufacture of a few other products, mainly vinegar. Official estimates put the size of this market at about 3’500 million litres. The remaining 1’000 million litres are systematically pumped out of wineries’ tanks – to take pressure off the market – into EU-subsidised distilleries producing ethyl alcohol of very little value.

Enlargement and WTO commitments may just spur the EU into the kind of radical action needed for balancing its wine market – an objective the Commission set out to achieve some 27 years ago [4]. Scrapping distillation altogether – a woefully inadequate measure in view of its ‘perverse effect’ [5] – would be the clearest sign yet that the EU is serious about reforming its wine policy.

May 18th, 2006

NOTES

[1] 0.7% per annum (2004-05 versus 1994-95, using 2-year averages), edging up to 0.9% over the last 5 years (2004-05 versus 1999-00). These growth rates are broadly consistent with trends prevailing last year, in spite of the data being reviewed by the OIV.

[2] 1.3% per annum, slowing down to 0.6% in the ‘noughties’ (as above). The Economist warned of looming overproduction in its December 1999 survey ‘The Globe in a Glass’.

[3] 3.2% pa, rising to 4.4% (as above).

[4] Commission of the European Communities (1978) ‘Progressive Establishment of Balance on the Market in Wine – Action Programme 1979-1985 and Report from the Commission’ in Bulletin of the European Communities, Supplement 7/78.

[5] The argumentation was made 18 years ago in The Common Wine Policy and Price Stabilization (Avebury/Gower, Aldershot, 1988, pp 125-33), by the author. Ten years earlier, the Commission had been cautioned against using distillation as a means of balancing the market, by its own financial services (EAGGF). To little avail: the measure was reinforced steadily, until Spain came into play, in the mid-1980s, then toned down as budget and international pressures grew. More recent evaluations of the measure have added nothing new to the debate but only served to confirm that distillation is indeed a huge waste of time and money.

© 2006 pierre spahni / www.span-e.com

You may quote or disseminate this article provided you make full reference to its author and website